ASV Scans: What they are, when you need them, and how they work

Learn what ASV scans are, when you need them for PCI compliance, and how Evervault simplifies the process with a modern, user-friendly solution.

By Shane Curran

Shane Curran

Shane Curran

Head of Compliance

For digital businesses accepting online payments, compliance with the Payment Card Industry Data Security Standard (PCI DSS) is mandatory. It’s a long standard with various requirements spanning the ways cardholder data is handled. Among these requirements are encryption standards, which safeguard data from unauthorized access.

Encryption requirements for PCI DSS compliance can become complicated, depending on how hands-on a business is with payment details (e.g., credit card data). This guide explores those requirements, detailing the challenges of implementing them alongside the practical strategies to maintain compliance.

The PCI DSS requirements outline strict encryption controls to ensure sensitive cardholder data is protected at rest and in transit. Generally speaking, they emphasize the use of strong cryptography and secure encryption key management practices.

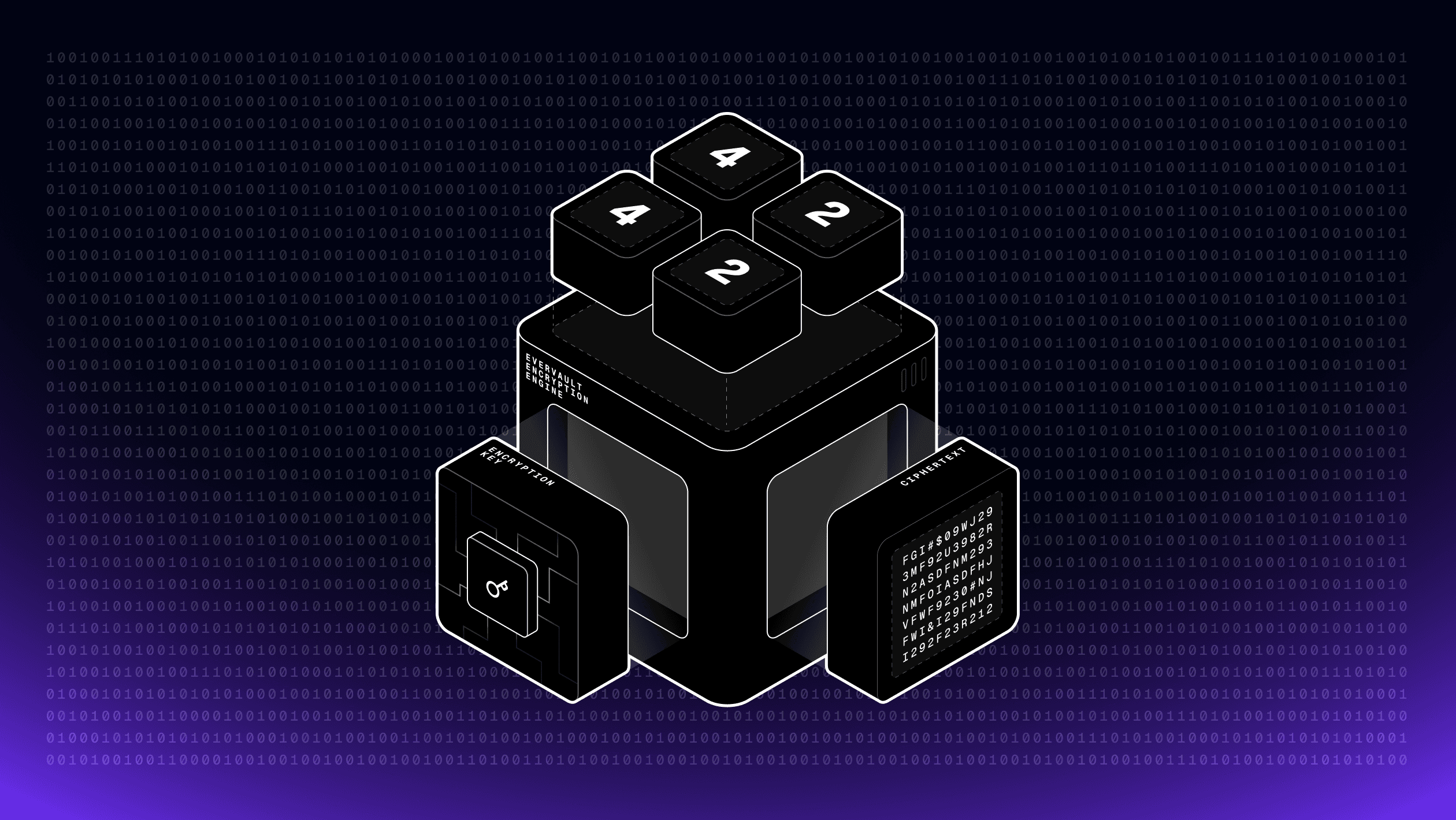

For some businesses, these controls aren’t relevant because they’re handled by a third-party product. For instance, businesses using Stripe and Stripe Elements experience little overhead as most concerns shift to Stripe. The same applies to customers using encryption services like Evervault; the encryption obligations (mostly) shift to the vendor’s engineering stack.

Encryption requirements remain mandatory, whether that’s to the end application or the third-party flow. To simplify things, we’ll first cover all the encryption controls detailed by PCI DSS, irrespective of who manages them. Then, we’ll touch on which of these could be outsourced to third parties, given the available tooling in 2025.

Let’s begin by discussing which encryption algorithms are recommended by PCI DSS to safeguard sensitive data:

By adopting these algorithms, businesses can ensure their encryption practices meet or exceed PCI DSS requirements.

Data in transit is highly vulnerable to interception, especially when transmitted across public networks. PCI DSS mandates strong cryptography to protect this data from unauthorized access.

These measures ensure that data remains secure during transmission, even when traveling across unsecured networks.

Stored cardholder data must also be encrypted to comply with PCI DSS. Unauthorized access to data at rest can lead to significant data breaches, making its protection critical.

These steps ensure that sensitive cardholder data remains secure, even if storage systems are compromised.

Encryption is only effective when encryption keys are properly managed. Poor key management practices can render even the strongest encryption useless. PCI DSS provides detailed requirements for cryptographic key management.

Proper key management not only enhances security; it also simplifies compliance efforts by demonstrating adherence to PCI DSS requirements.

Achieving PCI compliance often comes with technical and operational challenges. Recognizing and addressing these challenges is essential for smooth implementation.

These challenges underscore the need for strategic planning and resource allocation when implementing PCI DSS encryption requirements.

For organizations struggling to meet encryption requirements, alternative solutions can streamline compliance while maintaining robust security.

Tokenization replaces sensitive cardholder data with non-sensitive tokens, which have no exploitable value. Since tokens do not qualify as sensitive data, their use can reduce the burden of PCI compliance while providing strong security.

For companies accepting physical payments, P2PE encrypts payment card data at the point of entry (e.g., at a POI terminal) and keeps it encrypted until it reaches a secure endpoint, such as a payment processor, who maintains the private key used for decryption.

PCI DSS compliance is not a one-time achievement—it’s an ongoing process that requires continuous monitoring, updates, and testing.

Businesses should regularly update encryption protocols to address evolving threats. They should also conduct security audits, vulnerability scans, and penetration tests to identify and mitigate risks. Finally, they should monitor changes to PCI DSS standards and adapt encryption practices as needed.

Compliance isn’t just about avoiding penalties; it’s about maintaining customer trust and protecting against financial and reputational harm.

Encryption is fundamental to PCI DSS compliance, protecting cardholder data from unauthorized access and ensuring secure payment systems. By implementing robust encryption practices, managing keys securely, and addressing operational challenges, businesses can meet compliance requirements while safeguarding sensitive information.

Solutions like P2PE and tokenization offer practical ways to simplify compliance and enhance security. However, compliance is a continuous journey, requiring regular updates, testing, and monitoring.

Investing in strong encryption isn’t just about meeting regulatory standards—it’s about building customer trust, protecting the brand, and thriving in the digital payment ecosystem. By prioritizing security, an organization can confidently navigate the complexities of PCI DSS and foster a safer environment for payment transactions.

Learn what ASV scans are, when you need them for PCI compliance, and how Evervault simplifies the process with a modern, user-friendly solution.

Shane Curran

How Evervault’s dual-custody encryption model eliminates the fundamental limitations of traditional tokenization for PCI compliance

Shane Curran